2025 was supposed to be the year restaurants bounced back from inflation hell, but nope, enter bankruptcies, chef beatdowns, food poisoning lawsuits, and review-bombing wars that made Twitter look tame. From chains imploding to influencers tanking spots with one viral vid, the industry served up controversy on a silver platter. Buckle up for the top 10 moments that had everyone from line cooks to CEOs sweating bullets.

ICE Whiplash Exposes How Fragile Restaurant Labor Really Is

In the first half of 2025, ICE worksite enforcement became a constant background threat for restaurants. Under Trump’s second term, at least 40 worksite operations and more than 1,100 arrests were publicly reported across sectors like hospitality, agriculture, and food service, industries that run on immigrant labor.

Los Angeles turned into the symbol everyone else watched. Beginning June 6, federal immigration raids across LA County hit warehouses, car washes, public spaces and, earlier in the year, restaurant-heavy neighborhoods. Owners reported empty dining rooms, missing workers and sales drops in double digits, especially in Latino areas. Some closed temporarily because staff were too afraid to come in.

Then came the policy whiplash. On June 13-14, after heavy lobbying from business and agriculture groups, the administration quietly told ICE to pause raids on farms, restaurants and hotels, only to reverse that guidance a few days later and tell agents to resume operations. Restaurant associations and law firms scrambled to catch operators up: “know your rights” sessions, immigration-compliance webinars and ICE-raid checklists went from niche content to standing-room-only.

Bankruptcy Avalanche Reshapes Chain Dining

By late 2025, the numbers stopped looking like a “soft patch” and started looking like a reset. S&P Global data showed 655 large U.S. corporate bankruptcies through October, almost matching all of 2024’s 687 filings, and putting 2025 on track for the worst year since the aftermath of the Great Recession. October alone saw 68 big Chapter 11s, after 76 in August. By November, the tally had pushed past 700 companies, a roughly 14% jump year over year. Nypost

Restaurants weren’t at the top of the overall league table, but they became the most visible face of the crisis on Main Street. Casual-dining icons that defined the “mall era” spent the year either in court or in triage. Red Lobster, which filed for Chapter 11 in 2024 after closing more than 100 restaurants, spent 2025 shrinking its footprint and trying to reboot under new ownership and a tech-heavy “leaner” model. TGI Fridays, whose parent also hit bankruptcy at the end of 2024, entered 2025 by closing at least 36 U.S. locations and selling others to a new operator, with data services now tracking roughly 50–60 shuttered stores in this cycle alone. Hooters filed Chapter 11, promised its restaurants were “here to stay,” and then abruptly closed dozens of units; separate datasets suggest more than 100 closures tied to this restructuring wave.

Below that top tier, the body count kept rising. Industry coverage tracked at least nine regional or niche chains that filed for bankruptcy in 2025, from barbecue (Sticky Fingers) to Mexican (Abuelo’s, On The Border) to vegan concepts (Planta) and Italian groups like Bravo Brio and Bertucci’s. Some, like Planta and Abuelo’s, used Chapter 11 as a genuine restructuring tool and kept trading; others shut all remaining locations after years of slow decline.

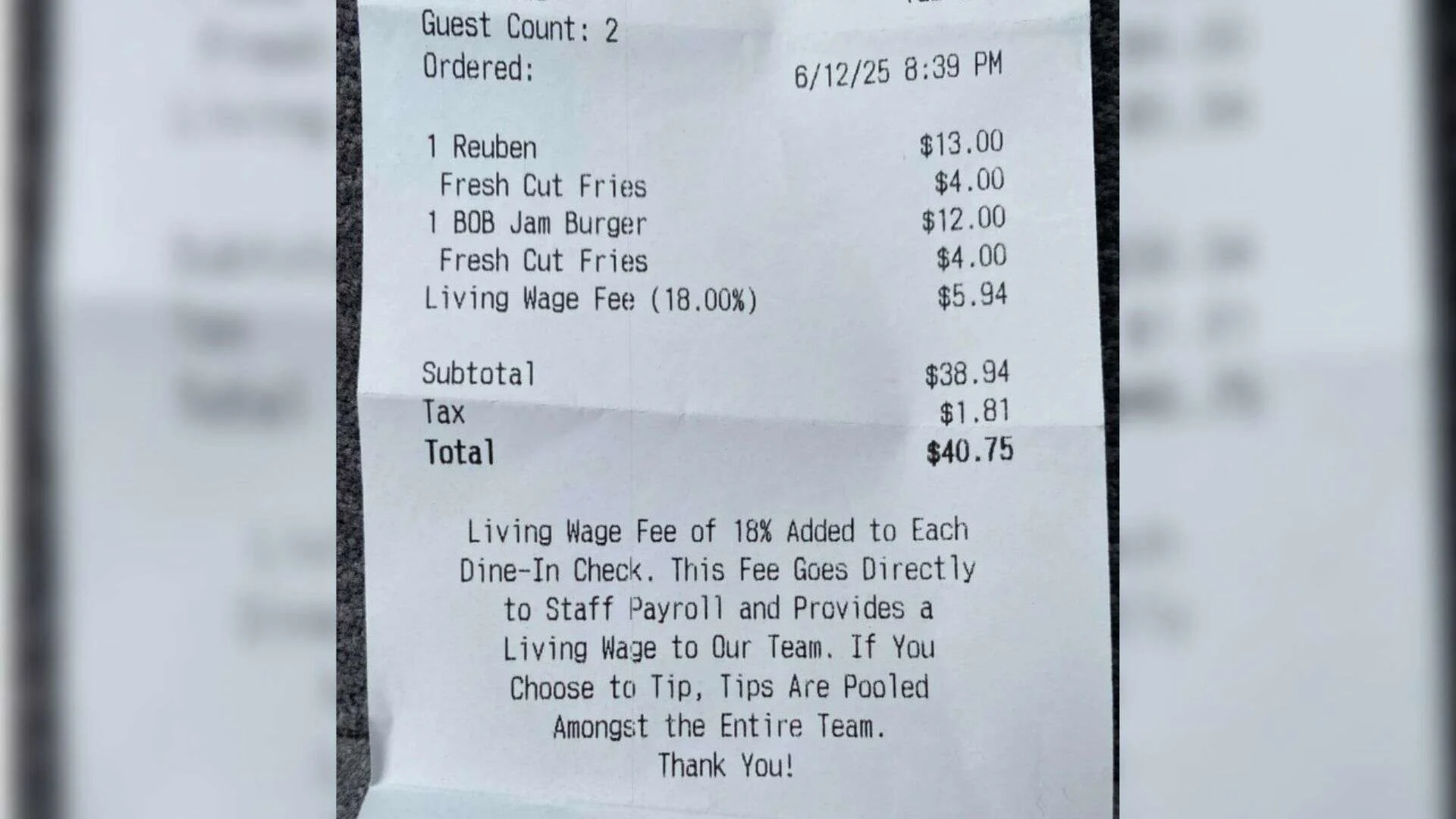

The 18% “Living Wage” Fee That Sparked a Backlash

In 2025, a single receipt – with an automatic “18% Living Wage Fee” tacked onto a pretty ordinary meal – set off a wave of anger on Threads, Reddit, and then mainstream media. Diners weren’t arguing about whether staff deserve a living wage; they were furious that a basic overhead cost showed up as a surprise surcharge at the bottom of the check. With a $17 Reuben already on the bill, the extra 18% felt less like fairness and more like being cornered into “forced tipping.”

The outrage landed on top of years of tipping fatigue. Americans are already nudged for tips at coffee counters, self-checkout, and takeout. Now guests were staring at a line that looked like an automatic gratuity, but was framed as “payroll”, with no clarity on whether they were still expected to tip on top. The message many people heard was: we’ll keep menu prices low on paper, then make you solve our wage problem in the fine print.

Some operators showed there’s another way. Places like Lula & Sadie’s in North Carolina openly add a living-wage fee and explain it everywhere: on menus, on the website, on the wall. Guests may still disagree, but they aren’t ambushed. The viral 18% receipt became a shorthand for the opposite approach, using fees as a back door instead of having an honest, upfront conversation about what it really costs to pay restaurant workers properly.

Global Food Fraud Surge Makes Your Pantry a Risk Zone

In 2025, “is this even what it says it is?” stopped being a food-safety nerd question and became a mainstream one. Food safety platforms like Digicomply and Authenticate reported that documented food fraud cases have jumped roughly tenfold over the past four years, with an estimated global cost around $40 billion a year. Fraudsters are riding the same forces operators are battling every day, climate shocks, wars, inflation, and tangled global supply chainsб and quietly swapping, stretching, or faking ingredients wherever they can.

The 2025 Global Food Fraud Index from FOODAKAI put hard numbers on where things are breaking. Nuts, nut products, and seeds are forecast to see fraud incidents up 358%; eggs +150%; dairy +80%; fish and seafood +74%; cocoa +66%. Herbs and spices, cereals and bakery, fats and oils, and even non-alcoholic beverages are all trending up too, with garlic showing up as a new hotspot for the first time. These are exactly the categories that power restaurant menus: pesto and desserts built on nuts, “premium” cheese, seafood specials, spice-heavy sauces, chocolate everything, plant milks, and bar mixers. The fraud patterns are boringly consistent, species substitution, origin fakery, and undeclared allergens hiding in stretched blends, but the risk lands squarely on the operator’s plate.

There was a little good news. Coffee, long a classic fraud target, is projected to see a steep drop in incidents, even as Starbucks spent 2025 fighting a lawsuit over “100% ethical” sourcing claims and alleged labour abuses in its supply chain. Juices, meat and poultry, honey, and fresh produce all showed modest declines in reported fraud. But the broader signal for restaurants was blunt: menu words and supplier specs are now reputational liabilities as much as they are marketing copy. 2025 is the year procurement teams, chefs, and legal finally ended up in the same meeting, talking about authentication testing, traceability tools, and which “too good to be true” deals to walk away from before they blow up on social or in a lab report.

DoorDash Gets Hacked, And Restaurant Tech Grows Teeth

In November 2025, DoorDash disclosed a major data breach after an employee fell for a social engineering scam. Hackers briefly accessed internal systems and saw personal data – names, addresses, contact details – for customers, Dashers, and merchants across the U.S. and Canada. No card or Social Security data was exposed, but restaurants still had to live with the fallout: nervous guests, breach notices, and the realization that a partner’s security lapse can instantly become their reputational problem too.

Meanwhile, the rest of the stack got smarter and more intertwined. Bites AI pitched a $1-per-order model that routes delivery through AI agents like ChatGPT straight into the POS; OpenTable rebuilt loyalty as OpenTable Regulars to steer repeat traffic; Grubhub rolled delivery robots into Jersey City; Menu-Order AI started matching GLP-1 users with “Ozempic-friendly” meals; and Toast launched Toast IQ, a conversational assistant wired into schedules, menus, and sales. The message for operators was hard to miss: as more of your business runs through connected platforms and AI, you’re not just buying convenience, you’re inheriting their security risk profile too.

Tariffs Turn Fresh Produce into a Moving Target

With Trump back in the White House, 2025 turned fresh produce into collateral damage in a rolling trade war. Tariffs and tariff threats on Mexico and Canada came and went within hours, but the signal to growers and importers was clear: nothing about cross-border pricing was stable anymore. By mid-year, Mexican berry exporters were warning that the U.S. habit of year-round strawberries, blueberries, and raspberries exists almost entirely because of Mexican supply, and that in the medium term, it’s the consumer who pays. The same logic applied to avocados, broccoli, cucumbers, peaches, mangoes, bananas and more: the stuff that keeps winter menus colorful suddenly depended on whatever was happening in D.C. that morning.

Upstream, Canada’s greenhouse sector, which ships 80–85% of its production to the U.S., called a proposed 25% tariff “dramatically consequential.” Texas importers said turning that tariff on would “close the valve” on winter fruits and vegetables at the border. Downstream, restaurants saw only the practical version: fewer SKUs, higher prices, and less room for aggressive seasonal LTOs built on imported produce. By November, the Supreme Court was hearing arguments on whether the administration even had the authority to impose some of these tariffs under emergency powers, and whether billions in refunds might eventually be owed. For operators, that didn’t solve the immediate problem. 2025 was the year you could write a menu on Monday and have your berry cost or cucumber availability blown up by a tariff headline by Friday.

Pizza Hut Put on the Block

In November 2025, Yum! Brands did something that would’ve sounded unthinkable a decade ago: it formally put Pizza Hut under “strategic review”, openly saying the brand’s full value might be better realized outside the company, up to and including a sale. In the U.S., which accounts for about 42% of Pizza Hut’s global sales, same-store sales have been falling quarter after quarter; Q3 2025 marked roughly the eighth straight decline, with global system sales down 1% and U.S. results even weaker. At the same time, KFC and Taco Bell – both leaning hard into value and snackable innovation – posted mid-single to high-single digit gains, making Pizza Hut look like the weak link in Yum’s portfolio despite its nearly 20,000 stores worldwide.

The problems aren’t just on spreadsheets. In the UK, Pizza Hut is shutting roughly half its restaurants as consumers drift to cheaper, faster, or more “modern” pizza competitors; in the U.S., Domino’s, Little Caesars and fast-casual upstarts keep grabbing share with sharper delivery, price points, and app experiences. What used to be a red-roof, salad-bar family ritual is now a brand stuck in the middle: too slow and expensive to win the value war, too legacy to feel exciting. The 2025 sale talk turned Pizza Hut into a symbol of a bigger shift, that even the most familiar chains are no longer “forever assets.” If they can’t prove their value proposition in a high-inflation, promo-driven market, they’re suddenly just another line item for a corporate portfolio review.

Ultra-Processed Food Goes on Trial

In late 2025, ultra-processed food finally stopped being just a “nutrition debate” and started looking like a global corporate accountability story. A three-part series in The Lancet, backed by UNICEF and the World Health Organization, pulled together 104 studies and concluded that ultra-processed foods (UPFs) are consistently linked to obesity, type 2 diabetes, heart disease, and early death, and that they now make up more than half of the average American adult’s calories.

The numbers behind the critique were brutal. Researchers found that over 50% of the $2.9 trillion paid to food-industry shareholders between 1962 and 2021 came from manufacturers of ultra-processed foods. Experts like Carlos Monteiro and Barry Popkin described how Big Food can “double or triple profits” by breaking whole foods down into a cheap base and rebuilding them with sugar, salt, fat, flavors, and additives “until they become irresistible”, hen defending that model with lobbying, influencers, and industry-funded science.

For restaurants, this wasn’t just an indictment of supermarket snacks. It was a shot across the bow of anyone leaning heavily on industrial sauces, frozen items, and branded “heat and serve” components to make menus work. With UNICEF and WHO openly calling for tighter global regulation of UPFs and countries from Mexico to the UK already restricting marketing to kids and taxing sugary products, 2025 marked the moment when “clean label” and scratch cooking stopped being a niche flex, and started to look like reputational risk management.

The GLP-1 Era Shrinks Portions and Redefines “Indulgence”

2025 was the year GLP-1 drugs stopped being a medical headline and became a menu problem. At the National Restaurant Association Show, consultants were no longer asking “if” these drugs would affect dining, but “how fast.” Roughly 12% of U.S. adults have tried a GLP-1 for weight loss, about 6%, around 20 million people, are currently on one, and interest runs at about 30%. For restaurants, the kicker is behavioral: GLP-1 users visit restaurants about 50% less often and 63% of them say they spend less when they do go out. Appetite, literally, is smaller.

They’re also eating differently. According to research shared at the show, GLP-1 users move from emotional eating to functional eating. They’re actively avoiding giant portions, sugary drinks, fried foods, salty snacks, heavy spice, and high-calorie alcohol. What they want instead: protein, nutrient density, fiber, low-carb, low-sugar options, whole foods, and smaller portions. The playbook that emerged in 2025 was clear: more starters, shareables, small plates and half portions (priced at roughly three-quarters), “luxury bites,” dessert flights, and all-day “snackified” items like cheese, nuts, jerky, veggies with hummus, guac, and protein-forward sweets. On the bar side, that means lighter profiles, mocktails, low-ABV cocktails, sparkling and herbal drinks, with sugar kept in check.

For operators, the GLP-1 wave is awkward: most users don’t want to be marketed to explicitly as “Ozempic diners,” but they’re already reshaping mix and check. In 2025, smart brands quietly rewrote their menus and marketing around benefit language, “protein-packed,” “fiber-rich,” “slow-burn energy”, and made sure nearly everything could be ordered in a smaller, still-premium format. The message from the stage in Chicago summed it up: this is happening whether the industry likes it or not. Ignore it, and you’re designing menus for an appetite your guests no longer have.

Wonder Buys Tastemade and Tries to Own “What You Watch” and “What You Eat”

In 2025, Wonder moved from ambitious delivery player to full-stack “mealtime platform” by acquiring Tastemade for about $90 million. The deal gives Wonder a food-first media engine with 160 million social followers, 13 million monthly streaming viewers, and 1,000+ hours of content, layered on top of Grubhub (delivery) and Blue Apron (meal kits). The plan is obvious: shrink the distance between watching a dish on your phone and getting something similar delivered, all inside one ecosystem.

For everyone else in restaurants, this is less about one M&A headline and more about a new type of competitor. Wonder is building a vertically integrated loop where the same company controls the food shows, the brands, the kitchens, and the last mile. If it works, “food media” stops being just marketing air cover and turns into the primary gateway that decides whose food gets ordered in the first place.

If there’s a useful way to read 2025, it’s probably this: stop waiting for “normal” to come back. Build for smaller checks from some guests and higher expectations from all of them. Be transparent about what things cost and why. Treat supply chains, data security, and labor models as core product decisions, not admin chores. And keep an eye on the players trying to turn food, media, logistics, and data into one integrated system, because the next “surprising” year in restaurants is likely to come from whatever they decide to do next.

To learn about more insights from the industry (and not only), you can subscribe to KitchenHub newsletter.

%20(20).png)